Watching your teenager get behind the wheel for the first time is an exciting milestone, but it also comes with new responsibilities. Because these new drivers have limited driving experience, it is especially important to help instill safe driving habits and understand your insurance options.

As your teen is learning to drive, consider these safety tips to encourage responsible driving habits.

Avoid electronics. Talk with your teenager about the importance of keeping cell phones, tablets, and other electronic devices out of reach while behind the wheel. In fact, the South Carolina Hands-Free and Distracted Driving law prohibits drivers from holding or supporting mobile devices with any part of their body while operating a vehicle.

Establish clear driving rules. Before handing over the car keys, discuss the driving dos and don’ts and set clear guidelines. It’s important to outline expectations for adherence to speed limits, cell phone usage, seatbelts, and curfews. You may also consider using driving monitoring apps, which can monitor location, speed, phone usage, and braking habits. Encouraging smart driving behaviors not only helps keep your teen safe but may also qualify you for discounts offered by some insurance providers.

Lead by example. Teenagers often learn driving behaviors from their parents. Practicing safe habits such as wearing a seatbelt, using turn signals, managing blind spots, and staying focused on the road can help set a good example for your new driver.

Limit distractions. Distracted driving is one of the leading causes of accidents among young drivers. Encourage your teen to enforce passenger limits, avoid eating or drinking, and wait to adjust the radio or GPS until they’ve come to a complete stop.

Practice driving in different conditions. The more experience your teens have, the more confident and prepared they become. Be sure to spend time practicing in a variety of different weather, traffic, and roadway conditions.

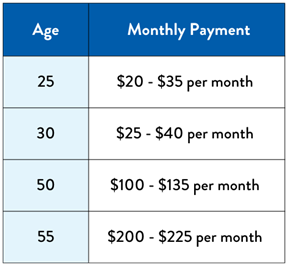

Adding a teen driver to your auto insurance typically increases your premium. Review your policy to understand liability coverage limits, deductibles, and available discounts for good students or driver education programs.

By setting clear expectations and ensuring your teen driver has appropriate auto insurance coverage, you can help them navigate the road with greater confidence and peace of mind. We can assist with determining coverage options and potential discounts that best fit your family’s needs. Click here or give us a call at (833) 359-0725 to get started with a complimentary insurance review!